How to lower Credit Card Processing cost

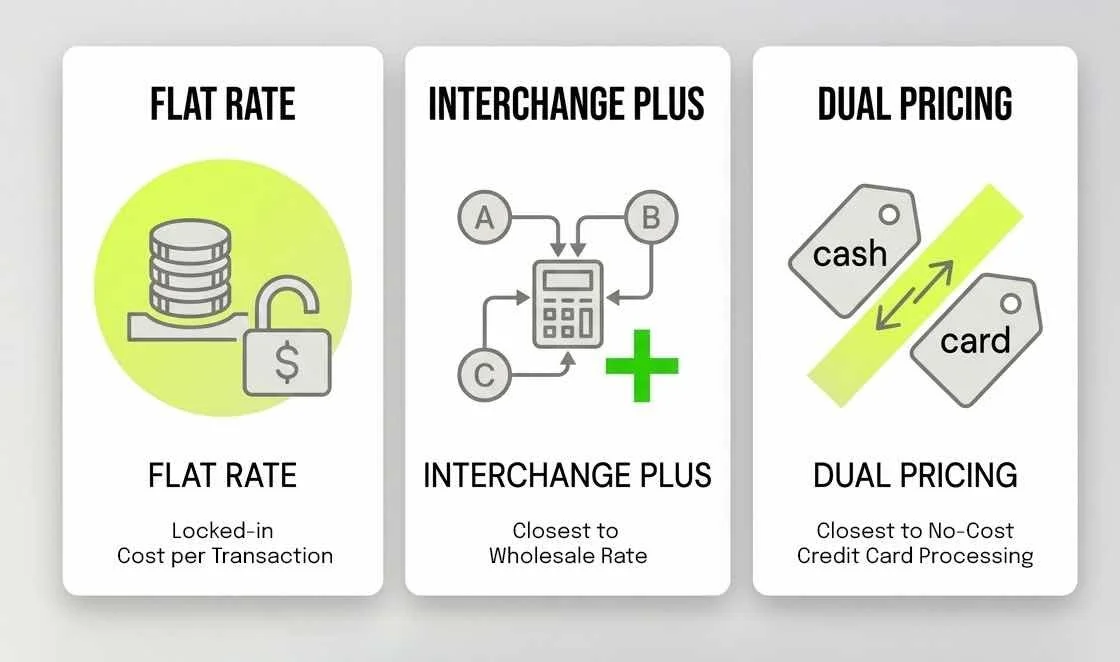

Selecting a Pricing Model

One of the most straight forward ways to lower your credit card processing is simple by selecting the right pricing model for your business. There is no single "correct" model; the right choice depends on your volume, how you capture card data, and whether you want to absorb costs or pass them to your customers.

Below is a breakdown of the three most popular payment processing services to help you decide.

There are plenty of pricing models in the industry, but these are the main three, and the ones we’ll focus on in this article:

Flat Rate Pricing: One Consistent Fee

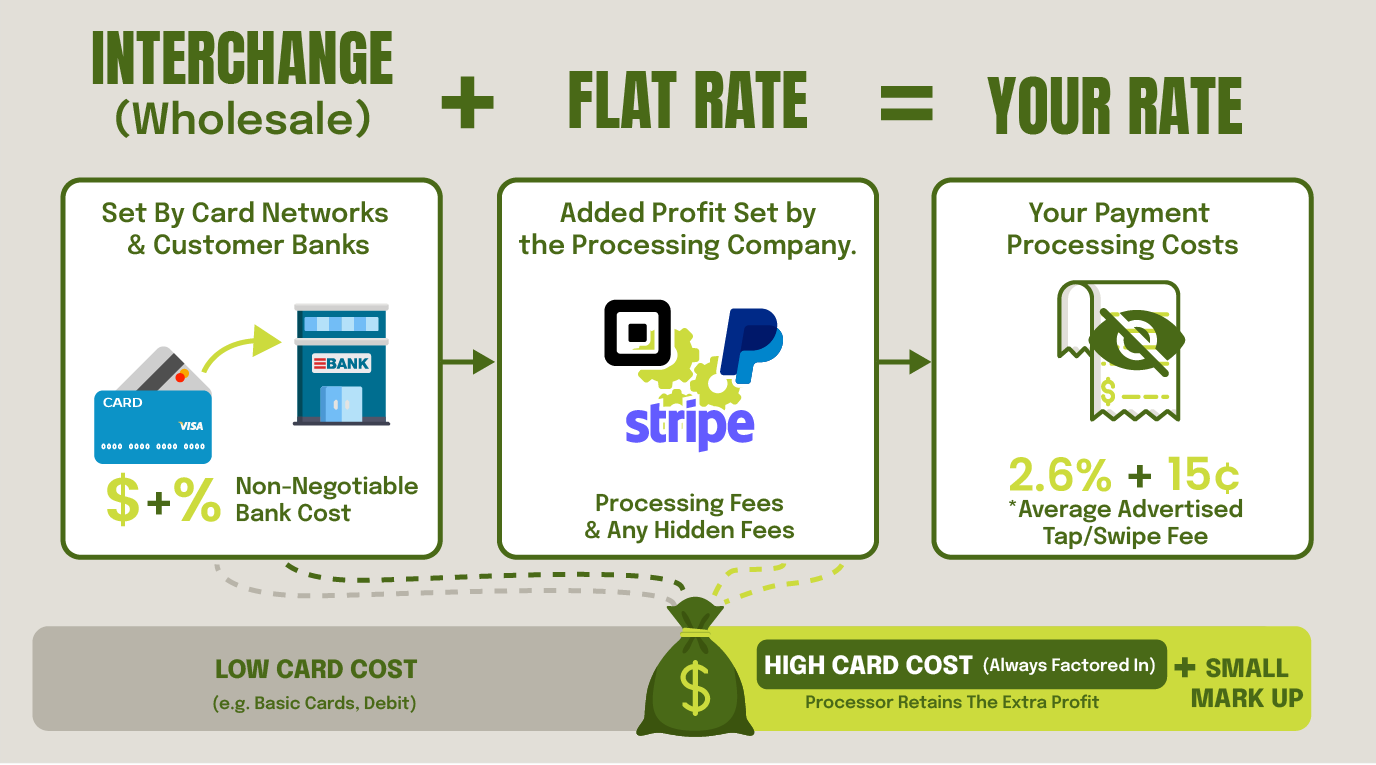

1. Flat Rate Pricing: Simple and Predictable

Flat rate pricing is exactly what it sounds like: you pay one fixed percentage for every transaction, regardless of the card type used.

How it Works: The processor combines the wholesale rate (interchange) and their processor markup into a single fee. Common examples include Square or Swipe, often charging around 2.6% + 15¢ for in-person "card-present" transactions. Those are the transactions taken in the store.

Pros:

It is highly predictable and makes merchant statement reconciliation simple.

You can also accept "elite" cards with high fees (like American Express) without paying extra because their average rate is already factored into the cost.

Cons:

It can be less transparent and often more expensive long-term for especially for high-volume businesses.

You don't benefit from lower-cost cards, such as debit transactions.

If you take in too many high-cost cards, your rate and fees will be adjusted to compensate for processor losses.

Is Flat Rate’s Simplicity Right for your Business?

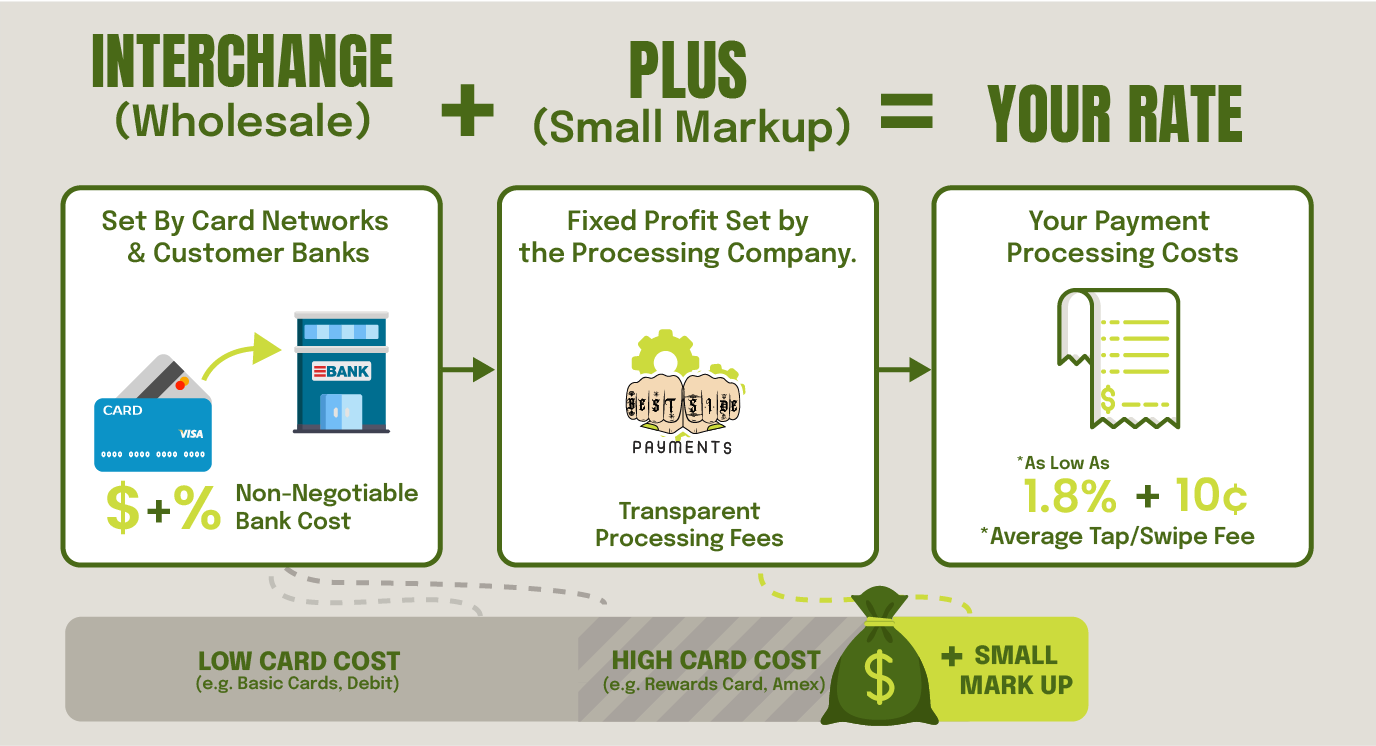

Interchange Plus: Transparent & Fair

2. Interchange Plus Pricing:

Often called the most honest model, interchange plus pricing separates the non-negotiable interchange fee (set by Visa, Mastercard, etc.) from the processor's markup.

How it Works: You pay the literal "at-cost" price from the card network plus a small, fixed fee to your processor.

Pros: This offers the highest level of transparency. If card networks lower their fees, those savings are passed directly to you. It is frequently the cheapest credit card processing option for growing businesses with high transaction volumes.

Cons: Your credit card processing statement will be much more complex. Because costs fluctuate based on the specific card used, monthly expenses are harder to predict.

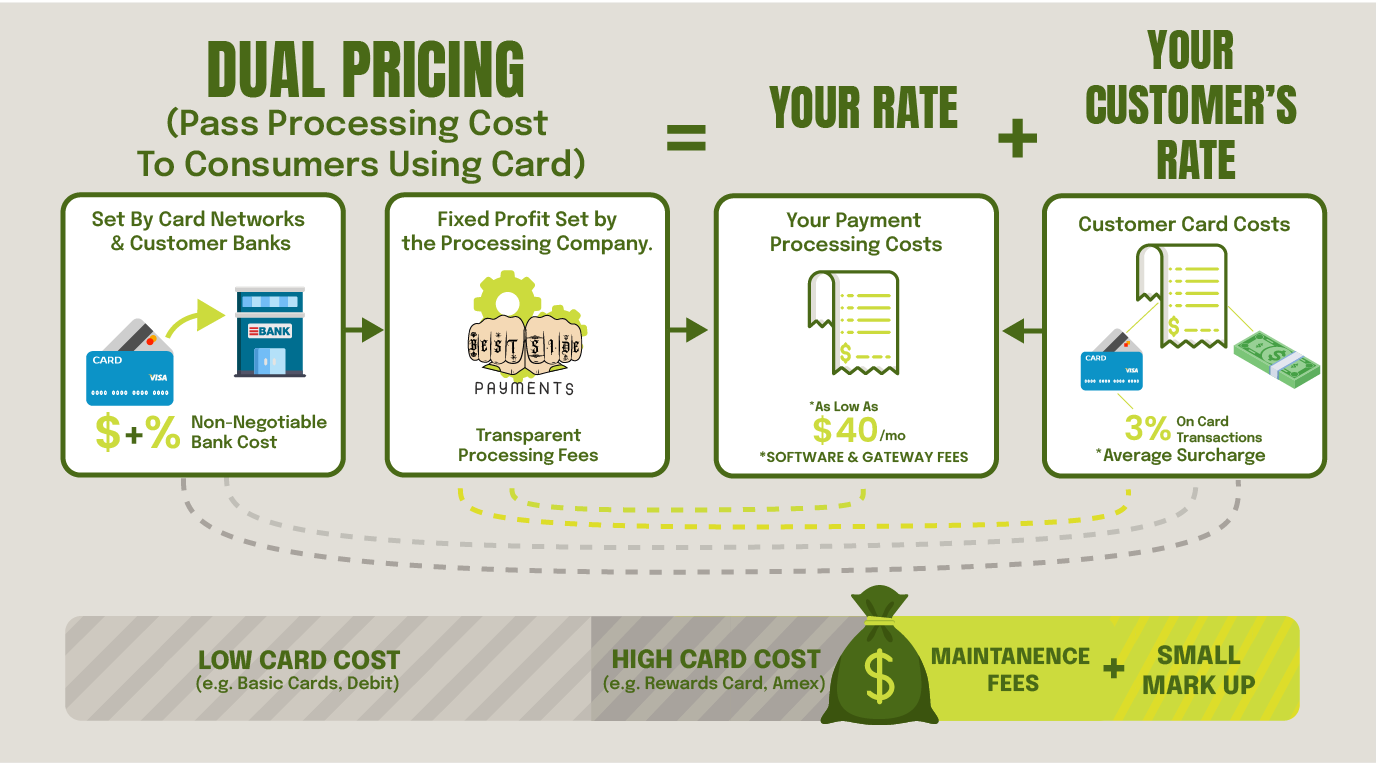

Dual Pricing: No-Cost Processing

3. Dual Pricing (Cash Discounting): Protecting Your Margins

For many, the best credit card processor for small business is one that eliminates processing costs entirely. Dual pricing and cash discount programs have recently become the "big opportunity" for merchants to protect their bottom line.

How it Works: *

Dual Pricing: You display two separate prices for every item—one for cash and one for card. Like a gas station, which displays both card and cash price.

Cash Discount: A subset of dual pricing, You list just one price: the "card price", and provide a discount if the customer pays with cash.

Pros: This model essentially results in zero fee credit card processing for the merchant, as the card-paying customer covers the cost of acceptance.

Cons: It requires clear, compliant signage and specific terminal setup to avoid issues with card brands like Visa. However this is what we can help you with so that you have a smooth transition.

Comparison at a Glance

| Feature | Flat Rate | Interchange Plus | Dual Pricing |

|---|---|---|---|

| Transparency | Medium | High | High (Upfront prices) |

| Cost to Merchant | Moderate/High | Moderate/Low | Near Zero |

| Predictability | High | Low (Fluctuates) | High |

| Best For | Low volume / New biz | Growing / High volume | Margin protection |

Which Structure Is Right for You?

If you want a no-cost credit card processing solution to combat rising inflation, dual pricing is your strongest bet. However, if you prefer to absorb the fees as a standard operating expense and want the most data-driven breakdown, interchange plus pricing is the industry gold standard for transparency.

Regardless of the model you choose, remember that card-not-present (online or keyed-in) transactions will always carry higher rates due to increased fraud risks. Always compare providers based on your specific total processing volume to find the most cost-effective path.

Does your business primarily take payments online or in person, or are you looking for the cheapest way to accept credit cards online? Let us do a free, no pressure review to help you minimize your credit card processing fees.

TABLE OF CONTENTS

Interchange Plus

Dual Pricing